Are you gearing up to dive into the Canadian real estate market? If so, you're likely facing one of the most crucial financial decisions: choosing the right mortgage term length. While the standard 25-year amortization has long been the norm in Canada, the option for a 30-year mortgage is increasingly enticing, especially with the recent policy changes.

Starting August 1, 2024, first-time homebuyers can opt for a 30-year amortization when purchasing newly built homes. However, this option isn't exclusive to newcomers. With a 20% down payment or by choosing an uninsured mortgage, you can also secure a 30-year mortgage. But before you decide, it's essential to weigh the pros and cons of smaller monthly payments versus paying more in interest over the life of the mortgage.

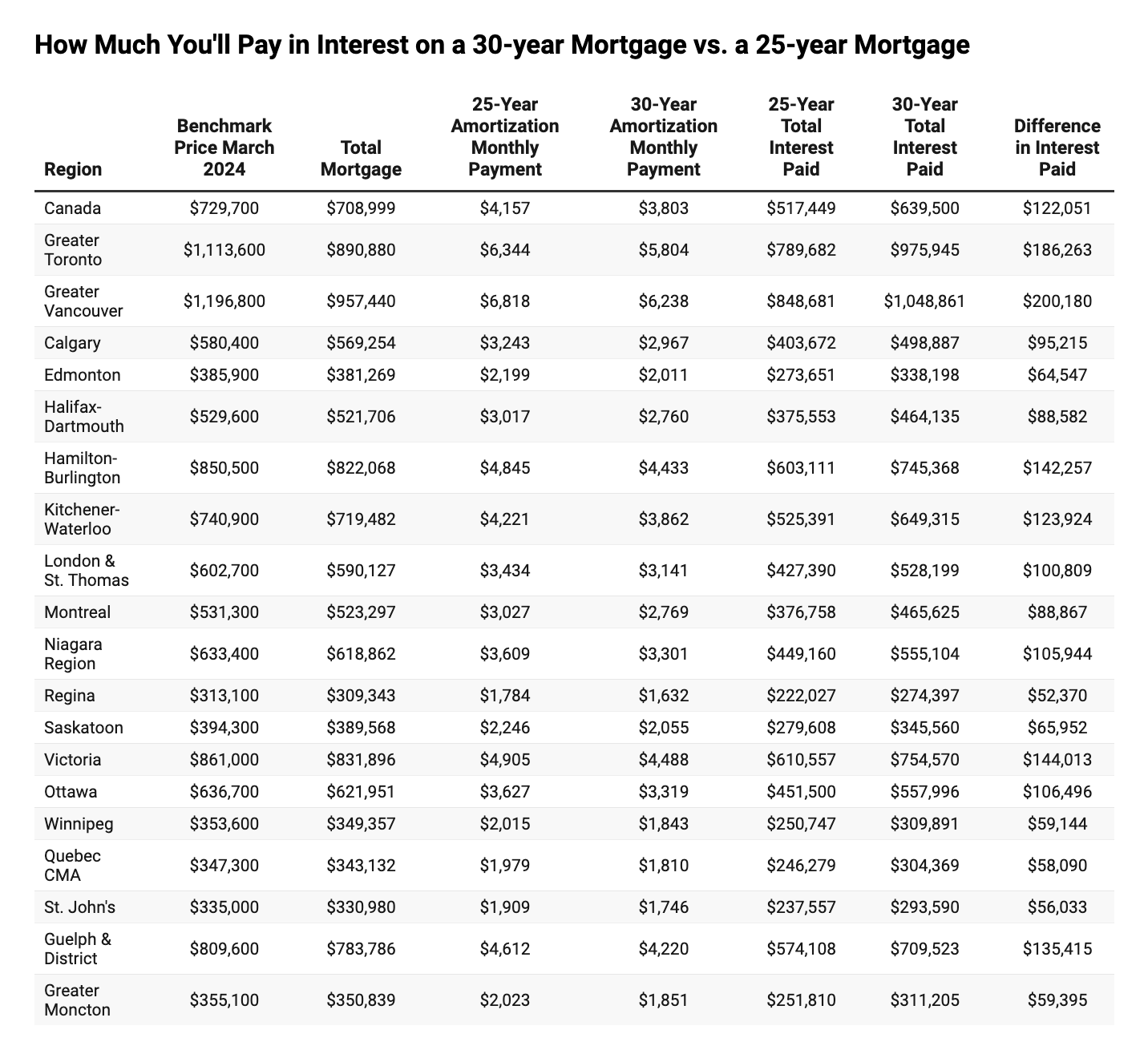

To shed light on this decision-making process, we conducted a thorough analysis across 20 Canadian cities. We compared the average monthly mortgage payments and total interest paid on a 25-year mortgage versus a 30-year mortgage, using a fixed rate of 4.79% and assuming a 20% down payment based on the most recent benchmark prices from March 2024. Source: Zoocasa

Source: Zoocasa

The Disparity in Interest Payments: A Closer Look

Unsurprisingly, cities like Vancouver and Toronto, with their soaring real estate prices, showcase the most significant disparities in interest payments between the two mortgage terms. In Vancouver, for instance, opting for a 30-year mortgage could mean shelling out an extra $200,000 in interest compared to a 25-year mortgage, despite the lower monthly payments.

Toronto follows a similar pattern, with homeowners potentially paying $186,263 more in interest over the mortgage period with a 30-year term. Other cities with notable differences in interest payments include Hamilton-Burlington, Victoria, and Guelph & District, all exceeding $125,000.

Impact Across Affordable Markets

Even in Canada's more affordable markets, the choice between a 25-year and a 30-year mortgage warrants careful consideration. Take Regina, for instance, where homeowners could save $52,370 in interest by opting for a 25-year term, despite the slightly higher monthly payments.

In cities like Moncton, St. John’s, Quebec, and Edmonton, where benchmark prices are under $400,000, the disparity in interest payments remains significant. Homeowners with a 30-year mortgage could end up paying over $55,000 more in interest compared to their counterparts with a 25-year term, with minimal differences in monthly payments.

Navigating the Canadian Real Estate Market

With the Canadian real estate landscape constantly evolving, making informed decisions about your mortgage is crucial. Whether you're eyeing a bustling metropolis or a cozy suburban enclave, understanding how your choice of mortgage term impacts your finances is paramount.

Reach out to us today to connect with an expert agent in your city and embark on your homeownership journey with confidence.