As housing prices and the cost of living continue to rise across Canada, finding ways to ease financial strain has become a priority for many. One powerful approach to improving your budget is by cutting back on non-essential expenses, with car ownership being a major one. With the average cost of owning a car reaching about $1,400 monthly—including payments, insurance, fuel, maintenance, and parking—Zoocasa explored how reallocating that money toward housing could make a significant difference for Canadian families.

The Benefits of Reducing Car Ownership

The Zoocasa report examined how downsizing from a two-car household to one, or even going car-free, could improve housing affordability across Canada. By analyzing average car-related expenses, Zoocasa illustrated how these savings could be redirected to help cover mortgage or rent payments. Mortgage estimates assumed a 25-year term with a 20% down payment and a 3.99% interest rate, while average rental prices were sourced from Zumper.

Monthly Car Ownership Breakdown

According to Autotrader, as of September 2024, the average selling price of a new car was $66,187. Statistics Canada reports that the average APR on new auto loans in October 2024 was 6.87%. Financing a brand-new car over an eight-year term would result in monthly payments of approximately $898.

Total Monthly Breakdown = $1,427

- Car payment:** $898

- Gas:** $250

- Upkeep:** $62.77 (seasonal tires, oil changes, cleaning)

- Insurance:** $95.23

- Parking:** $121

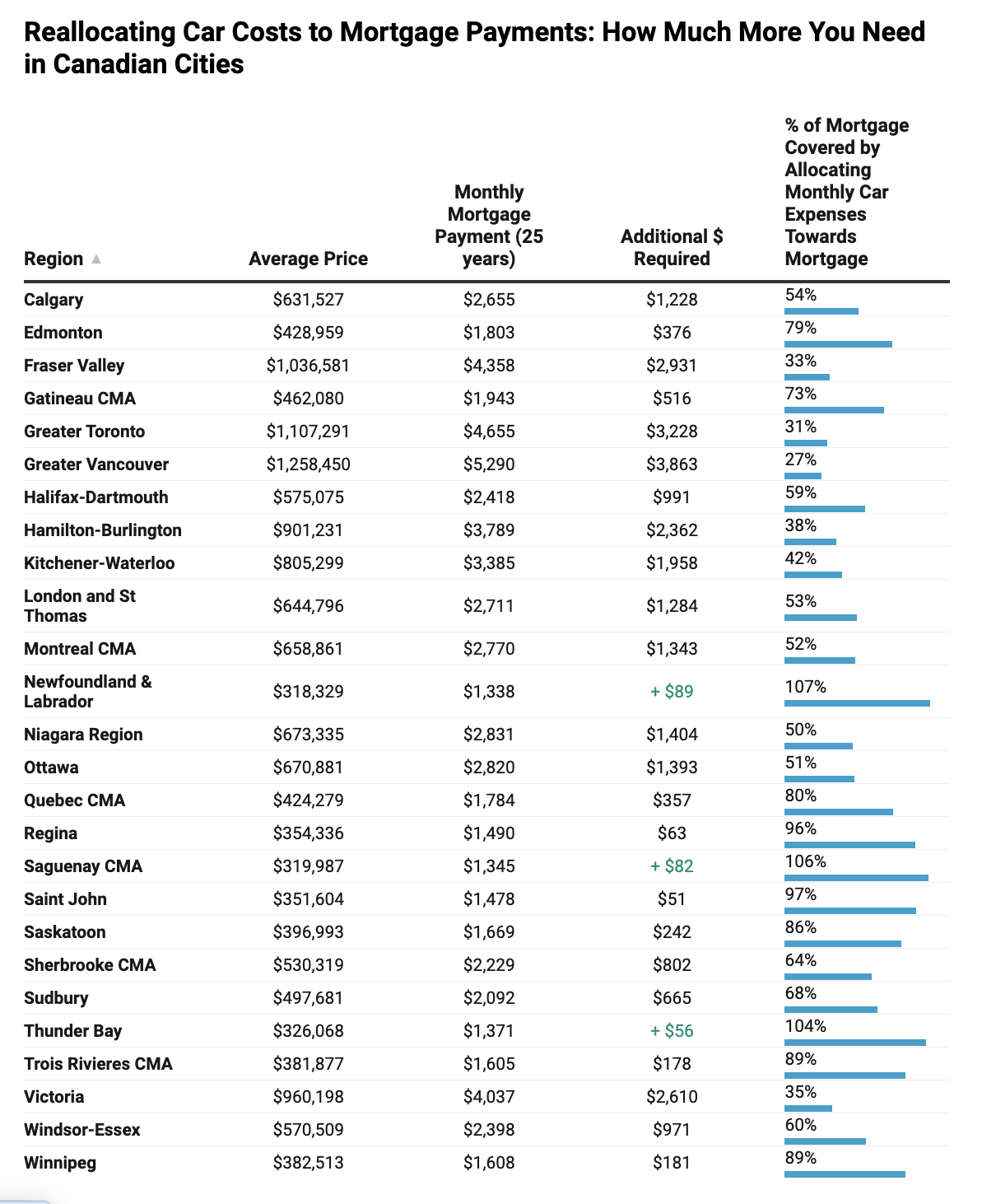

Zoocasa based mortgage calculations on a 25-year term, with a 20% down payment and a 3.99% interest rates.

Amount of money indicates an additionalrequired surplus amount.

How Forgoing Car Ownership Impacts Affordability

In 42.3% of the cities analyzed families that reduce from two-car to one-car households could save over 70% of their monthly mortgage costs. However, there’s a trade-off. While many of Canada’s most walkable cities have higher rents and mortgage payments, they also offer the convenience of reduced car dependency, making daily tasks easier without a vehicle. For instance, someone in Kitchener-Waterloo—known for its extensive public transit options and bike lanes—could manage without a car. Here, with an average home price of $805,299 and a monthly mortgage of $3,385, redirecting car expenses toward the mortgage would cover 42%.

In contrast, in the Niagara Region, where the average home price is $673,335 with a monthly mortgage of $2,831, utilizing car expenses for housing could cover 50% of the mortgage. However, the Niagara Region reports that residents without a car face mobility challenges, which could affect their quality of life. For families in car-dependent areas, sacrificing a vehicle might present more difficulties.

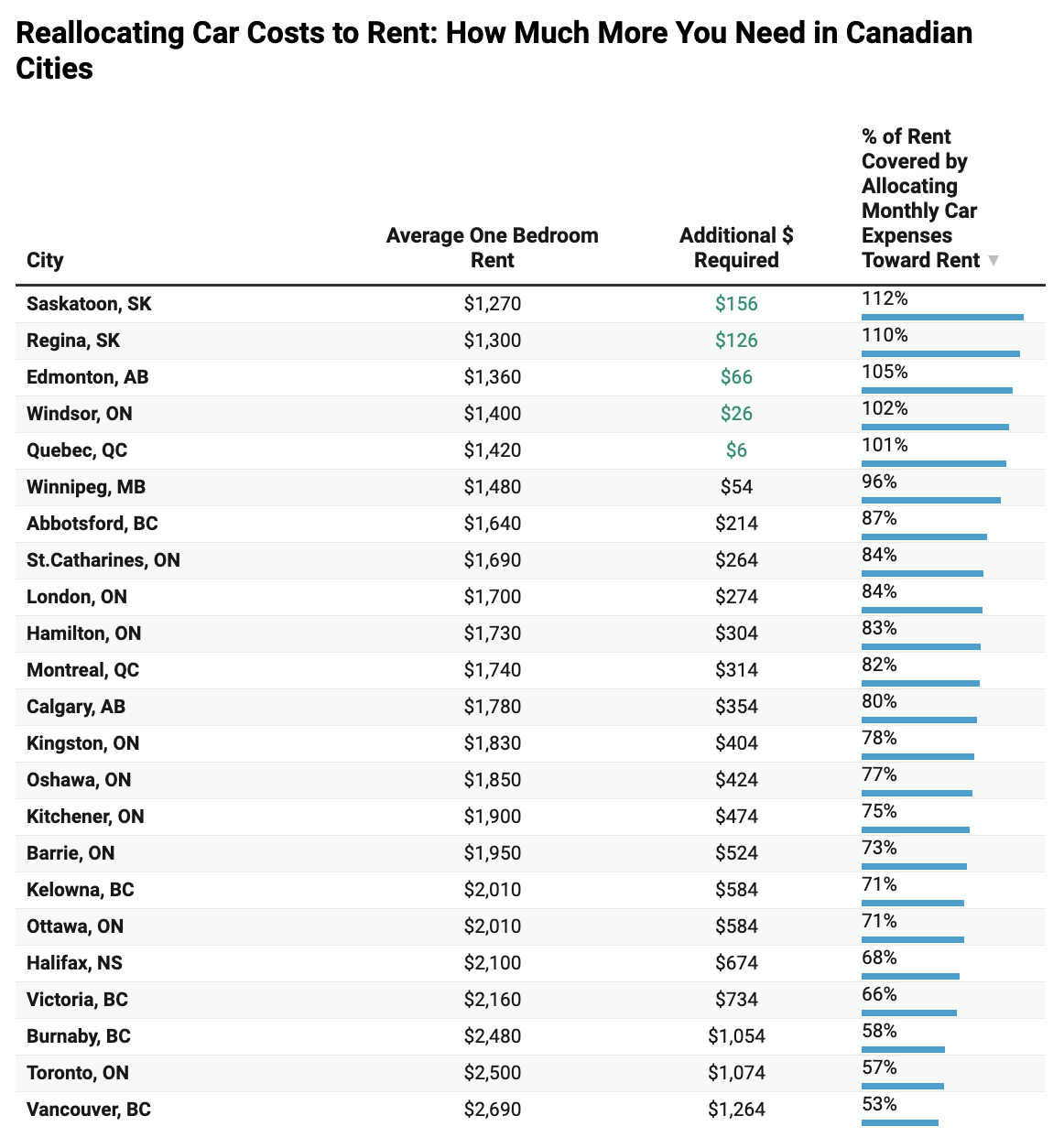

Average one-bedroom rents courtesy of Zumper. Average car expenses in Canada equal to $1,427 a month. Green text indicates a surplus amount after allocating monthly car expenses to rent.

Is Walking and Public Transit Feasible Year-Round?

In deciding where to live, transportation costs must be weighed alongside housing expenses. Car ownership is a major expense, but it may be necessary for certain regions with severe winter conditions that make walking or public transit challenging.

Consider Vancouver, where milder winter temperatures (around zero degrees) make walking more feasible year-round, despite higher housing costs. In contrast, Calgary often experiences winter temperatures as low as -30 degrees, making walking less practical. Financially, though, the impact of cutting car expenses is striking in Calgary—eliminating car costs could reduce a typical $2,655 monthly mortgage payment by 54%, bringing it down to $1,228. In Vancouver, where housing is pricier, the same savings would only reduce a $5,290 mortgage by 27%. While cutting car expenses doesn’t provide an immediate solution to high housing costs, it can still make a meaningful contribution to paying down the mortgage faster.

For residents in urban areas with extensive public transit systems, such as major Canadian cities, reducing car ownership is more realistic and can lead to significant savings. In Newfoundland & Labrador and Saguenay, for example, reallocating car expenses can cover over 100% of the typical mortgage payment—leaving a monthly surplus of $89. Other cities with similar savings include Thunder Bay (106%) and Saint John (104%).

Car Payments and Rent Costs in Major Metropolitan Areas

In Montreal, the amount spent on one car could cover 82% of a renter’s monthly housing costs, while in Toronto, it could cover 57% of the rent for a one-bedroom apartment. Reallocating car costs offers a substantial financial cushion that can go toward higher rent or faster savings for a down payment.

The Bottom Line: Making Smart Choices

Reducing car ownership and improving housing affordability largely depend on local public transit infrastructure and personal lifestyle needs. In transit-friendly cities, redirecting car expenses toward housing can help homeowners and renters alike manage their housing costs more effectively. This strategy can lead to smarter financial decisions, such as paying off a mortgage faster, building up a down payment, or investing in other assets.

Public transit infrastructure is vital for making car-free living feasible, especially for renters who benefit most significantly. Moving to more affordable, less car-dependent areas may help reduce overall costs. When considering a transition to car-free living, it’s essential to assess the available transit options and the convenience of reaching daily destinations without a car.